Is Non-Bank Lending for Me?

Dealing with the Big 4 Banks over the last five years and in particular post royal commission has been slow and a time-consuming process. The rates are low, so most clients are just used to “playing the game” to finally get some sort of approval (Sometimes). Is Non-Bank Lending the way forward?

Recent data has suggested that non-Bank lenders are forecasted to share some 35% of the commercial real estate (CRE) debt market by 2024. The Big 4 Banks once controlled nearly 85% of the market.

The market share of Australia’s big four banks (ANZ, NAB, CBA, and Westpac) fell during the June quarter of 2022, to 70.3 percent. The 10-year average is 78.2 percent. The big banks’ share of lending was 84.7 percent in 2013. So, who is taking the market share from the big banks? The Non-Bank sector is proving to be an option for many borrowers, as are smaller banks and second tiers.

Why Has Non-Bank Lending Become a Thing?

- Willingness to take more risk

- Faster loan approval process (2-3 days compared to 2-3 weeks with a bank)

- A less onerous application process and a tendency for a non-bank lender to view asset risk as the priority i.e Won’t get too tied up in wider group assets or other cash flow activities.

CRE Construction – Why Does Nil Presales / Nil Pre-leases Make the Transaction More Appealing

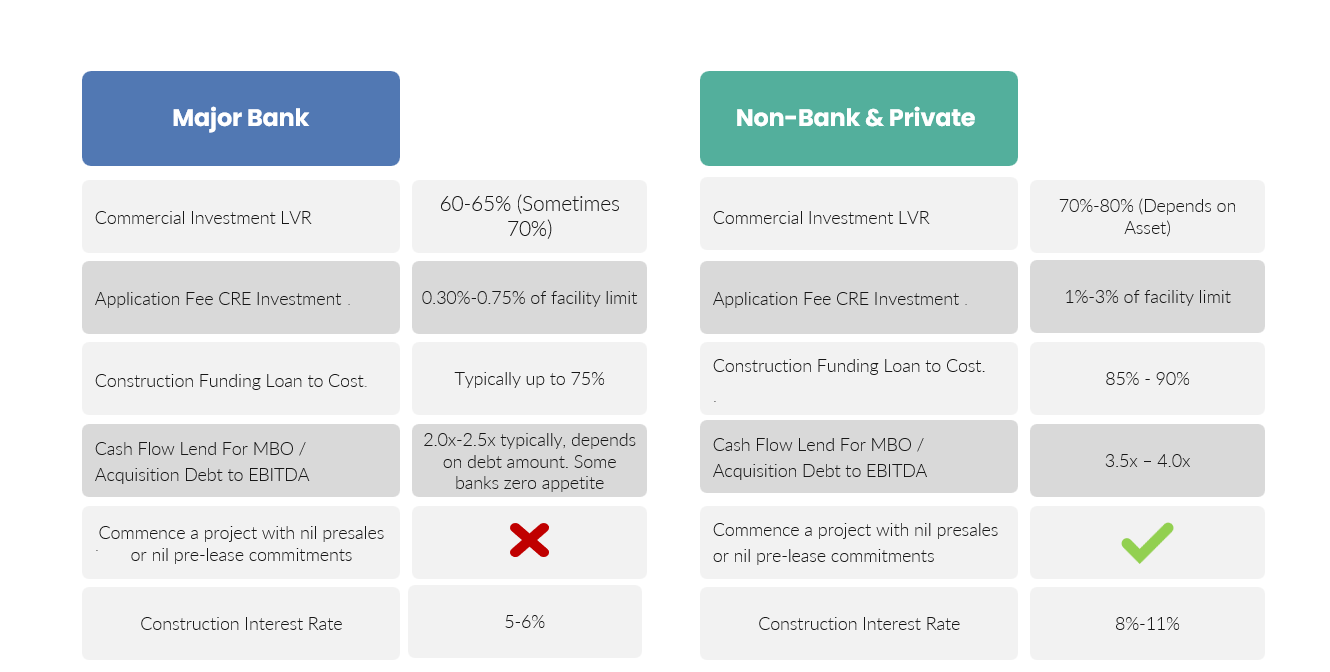

On a standalone project basis, big banks take next to nil risk and will rarely speculate. i.e you build a nice new office, they will want it pre-leased, you build a 10 townhouses development, they will be seeking a level of pre-sales which varies depending on the economic climate and quality of the project.

No presales and preleases can mean:

- More cash in the developer’s pocket at the front end of a project as marketing and presales commissions are not as important i.e less cash equity

- As the market moves and times change, holding stock provides flexibility to sell or lease at different rates or hold stock to take advantage of market movements

- And most importantly; the project can commence sooner without having to have qualifying presales or a prelease commitment, which means you avoid a rise in costs and take advantage of commencing other projects.

- Also, a lot of buyers like to ‘see, touch, and feel what they are buying (especially with large purchases such as property). Low or no pre-sales provide the developer with the opportunity to build the product and then sell it when buyers can inspect the property, often leading to a premium price.

Is Non-Bank lending only for property transactions or can my business borrow from a Non-Bank lender?

A common misconception is that non-bank lending is only for construction funding where developers are looking for more flexible conditions. Non-bank lending is also a large source of funding for traditional trading businesses. Much like non-bank funding for property transactions, the benefit often lies in the risk the non-bank lenders are willing to take. This is represented by aspects such as:

- Ability to leverage against the balance sheet & or cash flow without property security

- Lower cash equity contributions for acquisitions

- Greater willingness to have other funding arrangements as part of a transaction (eg. vendor finance, working capital funder, etc)

- More relaxed repayment profiles enable the business to build up cash reserves (rather than using all surplus funds for debt reduction)

- Non-recourse lending (no Director’s Guarantees)

Buyouts (MBOs)

An MBO is often viewed as a preferred option for a business owner as the continuity and a sense of “looking after the staff” are at times important to a business owner when looking at an exit.

The issue with an MBO, in particular one of a larger size and the $millions, is management teams won’t have the capital or security to execute the MBO, and traditionally this has meant vendor finance was the only option. Major banks in the SME space ($1m-$25M debt) are traditionally looking for tangible security and won’t leverage off historical and forecast cash flows if they do its traditionally very conservative leverage with a rapid payback period of 3-5 years.

A non-bank option for a buyout is a great option and deals can at times be structured at 3.5-4.5x normalised EBITDA, on a pure cash flow lend basis i.e. a non-bank won’t ask, “Can I have your house as security”?

Equity always comes into play and equity being contributed, cash being left in the business and the vendor finance arrangement is all analysed and factored into the overall deal metrics.

The advantage of a non-bank is we can structure facilities to work alongside other debt instruments and working capital facilities via inter-creditor agreements. Non-banks will always provide higher leverage over a major bank, and it’s important to factor in the total cost eliminating or reducing the equity requirements when considering a non-bank option, as the rates are often >10%.

Should I Consider Non-Bank Funding?

Non-banks are not subject to the same capital and regulatory requirements as banks, so this often means

- Often can speculate on earnings, and sales on development, or in general a more aggressive funding package is put together

- Non-bank funding costs are typically nearly double those of major banks, but the flexibility, ability for higher leverage, nil presales, and overall, often a quicker loan process is enough for a client to be attracted to a non-bank and private fund for capital.

- Developers can often be frustrated with their bank reweighting their CRE portfolios and this can mean a developer who specialises in industrial for example, their bank might “pull the pin” on industrial for 6mths as they are overweight in that asset class.

Non-Banks are now popping up everywhere, and as it is an unregulated world compared to a major bank, the options can be overwhelming for clients who perhaps are not active borrowers, and a lot of the smaller and more agile non-banks and private funders do not advertise their product offering, so the average person won’t know where to find the solutions to suit their needs.

Nexus Capital Partners are very active in the non-bank world, and we hold relationships with numerous players, and we can provide clients the full suite of options and illustrate the pros and cons.