Are Banks Finally Take More Risk?

Just under a year ago, we wrote an article about how interest rates affect borrowing capacity. Given the rate at which interest rates were climbing at the time, it highlighted how much the increase in rates over the preceding 12 months had eroded borrowing capacity. Since that time rates quickly climbed ~0.75% higher and have moved sideways since. With inflation remaining stubbornly above the target band, it now seems very unlikely there will be interest rate relief until at least early 2025. And in fact the latest data is suggesting that interest rates are more likely to actually go up again before they trend down. This has resulted in it becoming increasingly difficult for commercial real estate (CRE) clients, who are particularly sensitive to interest rate movements, to maximize the efficiency of their capital through gearing levels.

The Double Impact of Rising Rates & Stagnant Bank Policies

As rates climbed and then eventually plateaued post COVID, there was an expectation that there would be a softening of property investment yields which would allow for CRE borrowers to achieve the higher levels of gearing seen before and during COVID. i.e. a softening of yields would result in lower property values and therefore the same level of income could service a higher LVR under the same interest cover ratio policy (ICR = net income divided by interest). However, whilst there has been some softening of yields, particularly in lower grade assets, values for sought after asset classes (such as industrial and medical) in good areas with strong lease covenants have only marginally deteriorated, if at all. This has created headaches for borrowers because banks are very slow to move their policies and by not adjusting their ICR hurdle, it meant that each time interest rates went up, the LVR borrowers could achieve reduced. Fantastic for the banks given they were taking less and less risk. Terrible for borrowers who were forced to provide more and more equity to meet bank policies. At some point though the pendulum had to swing as banks need to lend money to make money and their policies were becoming too restrictive.

The Banks Finally Catch Up

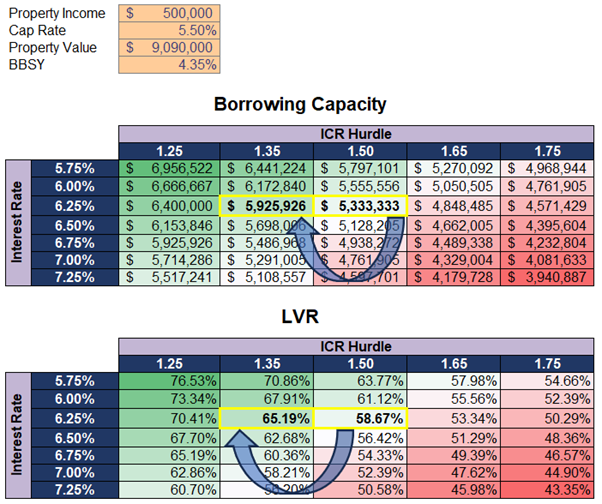

As mentioned above, banks need to lend money to make money. So it was inevitable that there had to be an adjustment to their policies as borrowers either weren’t looking to transact or they were exploring other options such as private credit, a fast-growing part of the market and a very real threat to banks. As a result, recently some banks have reduced their minimum ICR for CRE debt to 1.35x from 1.50x for certain asset classes. And given most banks have been pretty slow to move and therefore not transacting as much as they would like, there is currently quite a bit of heat in the finance market meaning some very attractive interest rates being offered (all up customer margins < 1.80% above BBSY). When the reduced ICR hurdle is coupled with an interest rate that reflects the risk profile (without the loyalty tax loading or any other reason for charging well above market), the impact on borrowing capacity can be significant. The below example illustrates the combined impact of interest rates and ICR hurdles and highlights how much a small change in the minimum ICR can affect borrowing capacity and subsequent LVR.

As can be seen in the above example, if a client is borrowing at 6.25% (pretty close to the market for quality assets and debt $5m+), a simple reduction in the minimum ICR from 1.50x to 1.35x increases their borrowing capacity by c. $600k. This translates to an LVR increase from 58% to 65%, a significant jump. Meaning the borrower can achieve the fairly standard maximum LVR for CRE debt with a bank. When reviewing the example taking into account a lower ICR hurdle and an interest rate reduction (which may be achievable if the credit risk margin is above market), the borrowing capacity can increase dramatically, particularly if the interest rate is towards the upper end of the range in the table.

So Are Banks Finally More Risk!?

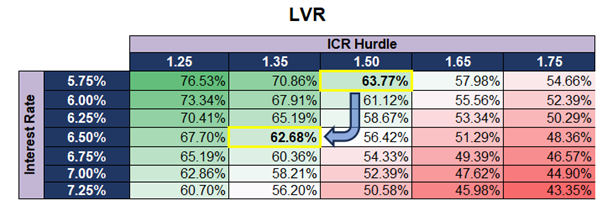

The above commentary regarding changes in banks’ policies might suggest that banks are finally starting to relax their risk settings and taking on more risk. The reality is, on the whole, this is probably not true (although for some asset classes or in some areas, they might be from time to time). Whilst it may appear they are relaxing their risk settings, all they are really doing is re-setting their risk levels to where they were before. If you compare the LVR movement based on the recent real life example of a 0.75% interest rate increase and a reduction of the ICR from 1.50x to 1.35x, as seen in the table below, the achievable LVR is actually lower! This is due to the increased interest costs outweighing the benefit of the ICR reduction.

So although some banks have recently moved their policies, they are effectively just re-setting them at levels from 6-12 months ago. And when banks are still only lending up to 65% for the best quality CRE assets, it could be argued they are still not really taking significant risk.

How Do I Find The Best Rate & The Most Appropriate ICR Hurdle?

Finding the best rate and the most attractive ICR hurdle can be difficult. The key is being able to access numerous finance options, understanding what each option looks like and introducing competitive tension. And you can only do this by working in the finance market each and every day. Whilst many property investors and business owners have a good understanding of the finance market, few have the time needed to continually explore all options to ensure they are getting the best deal. At Nexus Capital Partners, we focus solely on commercial finance. So we can confidently say we have a deep knowledge of what is available in the market and where best to place debt.

If this is something you would like to discuss or explore more, feel free to reach out to Nexus Capital Partners. We are experts in ensuring your finance arrangements are optimized ensuring not only you get the best deal, but you also don’t miss out on future opportunities.